Dollars cash money with note written 50-30-20 budget rule, concept of recommend saving rule – putting 50% toward needs, 30% toward wants 20% toward savings. Getty

Budgeting is fundamental to achieving financial stability and independence. While there are various methods, the 50/30/20 budget is one of the most popular, perhaps because it’s straightforward, easy to implement and highly adaptable.

This article highlights how the 50/30/20 rule works, what each number represents and why it’s a useful approach to reach your savings or investment targets. It also reveals how to adjust the percentages depending on your situation and includes example scenarios.

What Is The 50/30/20 Budget Rule?

50/30/20 is a guide for dividing your after-tax income, or the money that actually hits your bank account, into three categories: 50% for needs, 30% for wants and 20% for savings/investments. This is a baseline, so it’s not supposed to be rigid or perfect, but it’s meant to be simple and repeatable. Instead of building a budget from scratch every month, you can use this default split and adjust it based on your situation.

The buckets are straightforward. Housing, utilities, groceries and transportation fall under needs. Lifestyle choices like dining out, subscriptions, hobbies or other discretionary expenses are wants. The last category, savings and investments, is where you future-proof using retirement contributions, brokerage investing or extra debt payments.

For example, you have a $4,000 take-home pay this month. Following the 50/30/20 system, you allocate $2,000 to needs, $1,200 to wants and $800 to savings. This simplifies your budget and makes it easier to stick to. And since it includes discretionary spending, it feels less restrictive than other budgeting methods.

Why This Rule Is A Game-Changer For Investors

To succeed in investing, you need consistency, not perfection. As the saying goes : “Time in the market is better than timing the market.” The 50/30/20 rule helps because it turns saving and investing into a system. It quietly drives consistency by setting aside part of your earnings for long-term growth.

If you treat the 20% bucket as a non-negotiable, you force yourself to invest or save, not based on what’s left after spending, nor as an afterthought. You shift from asking “Can I afford to invest?” to “How do I want to invest this 20% I already planned for?” It now becomes a decision to either increase retirement contributions, build a portfolio, accelerate debt payoff or perhaps save for a down payment.

The rule also creates a healthy tension between today and tomorrow. Most budgets fail because they’re unrealistic — too strict, too fragile, too easy to abandon. 50/30/20 provides built-in room for enjoyment through the 30% bucket, reducing burnout. After all, a plan you can stick to beats a perfect one you quit after three weeks. As financial planner Julian B. Morris of Concierge Wealth Management advises, “Don’t feel like you have to be perfect. Perfect is the enemy of good. Good enough generally will win with consistency over time.”

Breaking Down The Buckets

50% For Needs

This covers the bills that keep your life running and your obligations current. Typical needs include rent or mortgage payments, basic utilities, groceries, insurance premiums, childcare, necessary medical costs, gas, car maintenance, public transportation and minimum payments on student loans or credit cards.

To know if something is a need, ask yourself: “Can I skip this item?” If the answer is no because it will create a problem, it falls under the 50% bucket.

Note that if your needs frequently exceed 50%, it’s a signal that something is amiss. Perhaps you’re house-poor, meaning your housing costs are crowding out other expenses. Or you might be in a high-cost area, supporting extended family or dealing with limited income. Whatever the case, the solution may be structural. You can renegotiate housing, downsize, refinance where appropriate, commute more or adjust insurance premiums. Try to shrink your needs before allocating more than 50% and reducing the other buckets. Of course, you can also increase your income .

30% For Wants

Wants include dinner dates, streaming services, gym memberships, planned vacations, takeout coffee, gifts, hobbies, the latest smartphone, concerts and even branded or premium versions of things you like. As mentioned above, this is where your budget becomes livable. Do not treat it as waste because it’s an important part of what helps you sustain and stick to your plan.

When used well, the 30% bucket creates a controlled environment for enjoying your money. You can spend freely without guilt or jeopardizing your goals, as long as you stay within the limit. This is crucial because lifestyle creep can be subtle: a few upgrades here, an additional subscription there, and suddenly there’s nothing left to invest. Be intentional with your spending, but spend. You don’t have to be miserable while saving for the future.

20% For Savings And Investing

This is your power bucket, especially if you want to build wealth. It includes developing an emergency fund, contributing to 401(k)s or IRAs, investing in brokerage accounts for long-term goals and paying down debt faster. It can also include sinking funds for predictable future expenses, such as car repairs, insurance premiums, children’s education or your long-term care requirements, because those reduce the need to rely on credit later.

Treat the 20% as a goal and don’t be discouraged if you can’t afford it yet. “Some feel that 20% is out of reach and therefore don’t save what is possible for them,” says Cole Williams, CFP, of Vessel Financial Planning. “If you can save 5%, great! If you can do 10% without meaningful quality of life changes, excellent! The point is to save what you can, and to make as much of this behavior automatic,” he adds.

What’s key here is to prioritize. Ideally, you build your emergency savings first, with six months’ worth of living expenses kept in an accessible account. Then, depending on your situation, you can target your debts, especially high-interest ones like credit cards . Or you can start retirement savings and aim to contribute enough to trigger the employer match , if available. Once these are set, you can expand your goals to perhaps early retirement or business ownership. A core element of the savings and investments bucket is to make your money work for you, and with time and compounding, it is possible. If you want to ensure saving or investing is not optional, automate and treat this bucket as a monthly bill or payment for your future self.

Adjusting The Rule To Meet Your Needs

Remember, the 50/30/20 rule is a starting point, not a law. Your circumstances may require a different split, and that doesn’t mean you’re doing it wrong. For example, many households can’t keep needs at 50% in the short-run, particularly in areas like New York City or Los Angeles, where the cost of living is higher. In such cases, a split like 60/25/15 can be a realistic bridge while you work on structural changes: higher income, housing change or debt reduction. But the goal is still the same: keep needs contained, preserve some lifestyle breathing room and build a consistent savings habit.

You may also adjust the rule upward if you have ambitious goals. For example, if you’re pursuing FIRE (Financial Independence, Retire Early), you can choose 45/20/35, shifting funds to savings and investments while keeping needs and wants tighter. This obviously requires additional sacrifice on your part, but it’ll be worth it to retire sooner.

If you have variable income, say you’re earning through commissions, freelance work or seasonal business revenue, you can set percentages based on an average month, then use the high-income months to overfund the savings bucket. Whatever the case, the best adjustment is the one you can sustain. If your plan is so aggressive that you quit, it’s worthless. Start with a split that works for you, implement for 60 to 90 days, then refine. Use this as a feedback loop: track, learn, refine, repeat.

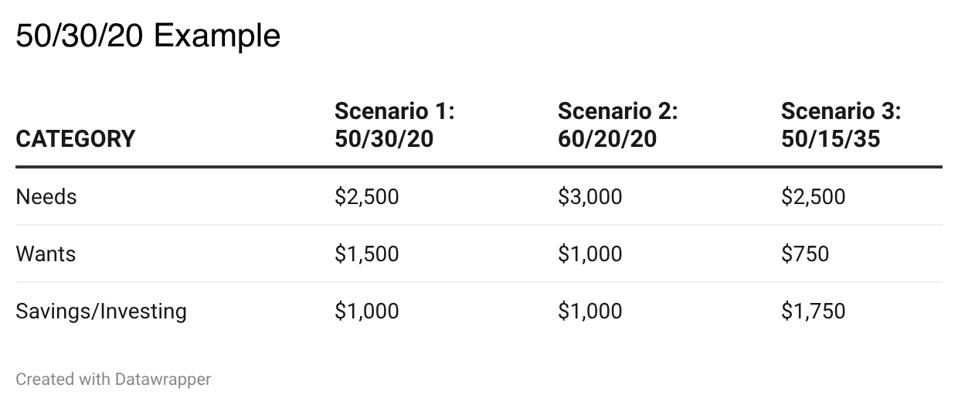

50/30/20 Practice Example

Consider these simple scenarios using $5,000 in after-tax monthly income. The baseline is 50/30/20, with $2,500 for needs, $1,500 for wants and $1,000 for savings/investments. If you live in a high-cost area and your needs are $3,000 (60%), adjust by shrinking wants while maintaining savings.

Or if you’re chasing a major goal, you can do the opposite: keep needs stable, trim wants and increase savings. You might do a 50/15/35 split, allocating the extra $750 to accelerate debt repayment or retirement savings.

50/30/20 Example

True Tamplin

The buckets stay the same: needs, wants, savings/investing. The percent allocations may change depending on your priorities, what works best and is sustainable. Feel free to play around with this as you apply the rule.

Bottom Line

The 50/30/20 budget rule works because it’s simple, flexible and consistent. You cover the essentials and pay your future self while allowing room to enjoy your money each month. Use it as a baseline, automate the savings bucket and adjust the percentages when your life and circumstances demand it. For further information and tailored guidance, consult a financial advisor .

© 2026 Forbes Media LLC. All Rights Reserved

This Forbes article was legally licensed through AdvisorStream.